Mortgage Backed Securities Default Rate

Mortgage Backed Securities Held By The Federal Reserve All Maturities Discontinued Mbst Fred St Louis Fed

Mall And Hotel Loans Are Blowing Up Commercial Mortgage Backed Securities Finanz Dk

Which U S Bank Is The Largest Holder Of Mortgage Backed Securities

Residential Mortgage Backed Securities And The To Be Announced Tba Market

Rmbs Issuance In The U S 2019 Statista

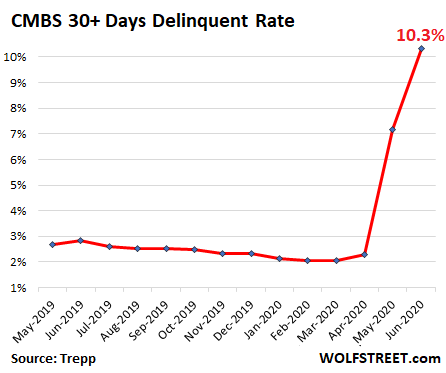

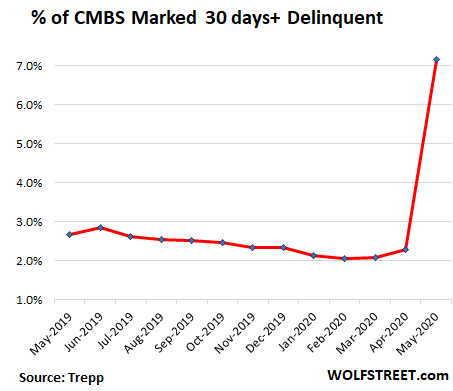

Cmbs Delinquency Rate Spikes By Most On Record Finanz Dk

In turn their prices tend to decrease at an increasing rate when rates are rising.

Mortgage backed securities default rate.

When The Qe Music Stops Us Mbs Will Still Be Dancing Investors Corner

U S Mortgage Delinquency Rate 2000 2018 Statista

Rem 2008 Repeat Risks Growing In U S Mortgage Market Bats Rem Seeking Alpha

Treasury And Agency Securities Mortgage Backed Securities Mbs All Commercial Banks Tmbacbw027nbog Fred St Louis Fed

Source : pinterest.com